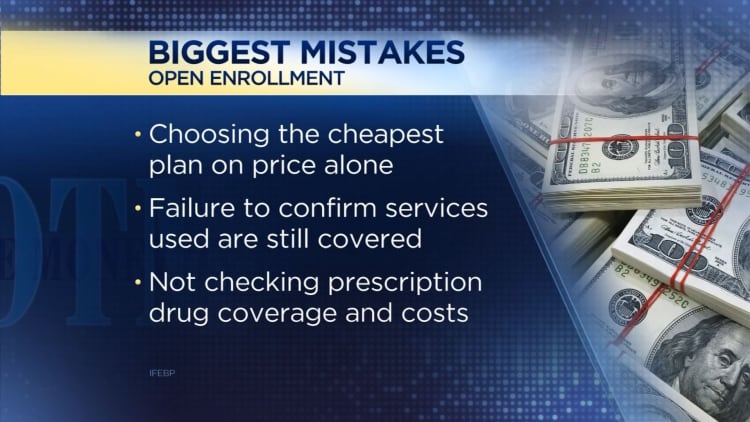

Pop quiz: What is the out-of-pocket limit for your health plan in 2018? How about your deductible?

These two figures are among six that will determine whether your plan will bust your budget next year.

"These figures can be tweaked each year by your employer or your plan to keep pace with healthcare expenses," said Brian Marcotte, president and CEO of the National Business Group on Health, an organization that represents large employers.

"Pay attention to see if there are any changes and see how that may impact the healthcare that you need," he said.

We're in the thick of open enrollment season — that time of year when workers select their health insurance plans and other employee benefits for 2018 — so keep an eye on these six numbers when you enroll.

Copayment

Your copayment is the amount of money you pay each time you visit a doctor or purchase a prescription drug. It's a form of cost-sharing with your insurer.

In 2015, employees paid an average of $139 toward co-pays, down from $218 in 2005, according to an analysis by the Kaiser Family Foundation.

"Money spent on co-pays is going down because fewer people have them," said Matthew Rae, senior policy analyst at Kaiser Family Foundation. Instead, health insurers and plans are using coinsurance to split costs with employees, charging them a percentage of the cost of service, rather than a flat dollar fee. (Click on graphic to enlarge.)

Coinsurance

Coinsurance can kick in once an employee reaches his or her deductible for the year. From that point, the insurer usually will cover a percentage of the cost of service, while the employee pays the rest.

"You're generally better off with a copay than you are with coinsurance," said Rae. "Coinsurance can add up to a lot of money very quickly."

For instance, on average, employees are on the hook for 19 percent of the cost for a hospital admission in 2017, according to data from Kaiser Family Foundation. Meanwhile, the average co-payment for a hospital visit is $336 per admission.

Deductibles

Once you've hit your plan's deductible, your insurer begins covering your costs.

Employers are sharing more costs with workers by bringing in high-deductible healthcare plans, which leave employees responsible for a greater share of upfront medical costs.

This year, workers with employer coverage can expect to pay a median of $1,500 before they meet their in-network deductible, according to an August 2017 survey of large employers by the National Business Group on Health.

That number goes up to $3,250 for family coverage.

Often, family plans have both individual and family deductibles, so keep track of them.

Employer contribution to health savings accounts

If you're in a high-deductible plan, you will likely be offered a health savings account to help you cover your costs.

This account has a triple-tax advantage: Contributions you make to your HSA are tax deductible or pretax, your balance accrues interest tax free, and your withdrawals are free of taxes as long as you're using the money for qualified medical expenses. The current version of the GOP tax plan continues those breaks. (Click on graphic to enlarge.)

Employers can help defray the cost of care by seeding HSA accounts. Workers in these plans receive an average employer contribution of $608 for single coverage and $1,086 for families.

This year you can contribute up to $3,400 to your HSA if you have single coverage or $6,750 for family coverage. Savers 55 and older can contribute an additional $1,000.

Out-of-pocket maximums

This is the most you'll have to pay for your covered services, including your co-pays, coinsurance and deductibles. Once your expenses have hit this threshold, your insurer generally will foot the bill for all of your costs as long as you see in-plan providers.

Be aware that under a family plan, you may have out-of-pocket maximums for your family overall and for each individual.

Under individual coverage, out-of-pocket maximums are typically $3,500. They are $7,075 for family coverage, according to the National Business Group on Health.

Premiums

Premiums your employer pays are exempt from federal income and payroll taxes. At the same time, the share you pay is excluded from your taxable income. The GOP tax plan released so far continues that.

Next year, employers expect to spend $8,527 per enrolled employee, according to data form the National Business Group on Health. Meanwhile, workers themselves will contribute an average of $2,752 toward their premiums.

WATCH: What you should know during open enrollment